Garage Door Depreciation Life

Https Pgelawsuit Com Wp Content Uploads 2017 12 Personal Property Claim Guide Pdf

Http Bensonaccountants Com Wp Content Uploads 2016 09 Rental Depreciation Checklist Pdf

Some Important Tips To Consider Best Garage Door Opener Needs A Repair

Answered Consider The Following Project For Hand Bartleby

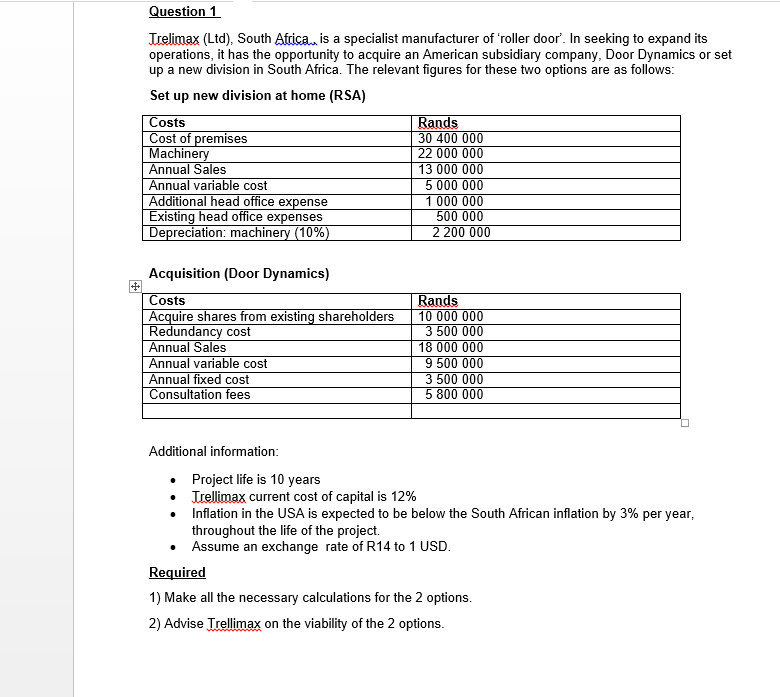

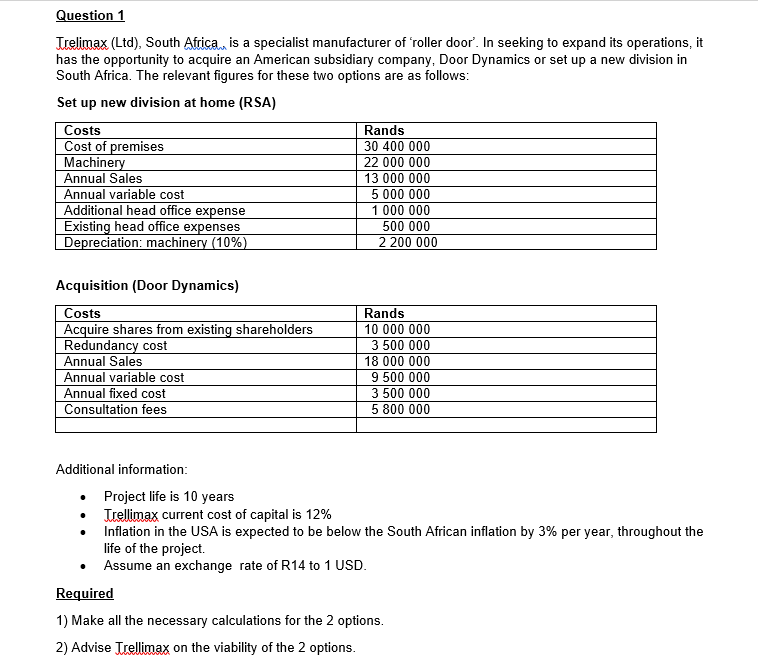

Solved Question 1 Trelimax Ltd South Atrica Is A Spec Chegg Com

What Is A Depreciation Report Why Is It Important Mcinnes Marketing

However under new de minimis rules you are able to deduct the entire cost in the year of purchase.

Garage door depreciation life.

Garage Door Repair Alpharetta Ga Archives Garage Door Experts

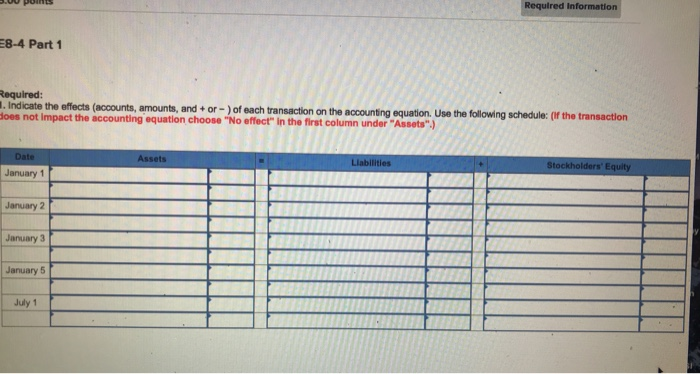

Solved E8 4 Determining Financial Statement Effects Of An Chegg Com

Cost Segregation Saving You Money On Self Storage Door Replacements

Https Www Overheaddoor Com Documents Rolling Service Door Systems Brochure Pdf

Why Depreciation Is A Landlord S Best Friend

Depreciation Schedules Services

Make Shed From Plans Agustus 2016

The Post Move Starting A Fresh Lifestyle The Savvy Scot Saving Money Best Money Saving Tips Weekly Saving

Solved Uestion Trelimax Ltd South Africa Is A Speci Chegg Com

Roof Insurance Claim Process Questions Bob Behrends Roofing Gutters

Underground Parking Royalty Free Images Stock Photography Ssuaphoto Window Architecture Bankruptcy Barrier Booth Building Business Car Che V 2020 G Komfort

How To Maximize Real Estate Tax Deductions Anderson Advisors

Walker Garage Door Garage Door Service And Repair Conroe Tx

Want To Claim Taxdeductions Using Property Investment Recently The Australian Government Changed Legislation Weatherboard House Hamptons House Facade House

How To Do Safety Inspection On Your Garage Door Garage Door Opener System Net

Online Business

Office Of Landlord Tenant Affairs Pdf Free Download

Download Empty Shop At Night Royalty Free Images Stock Photography Office Interior Modern Urban Ceiling In 2020 Street Stock Stock Photography City Streets

Https Encrypted Tbn0 Gstatic Com Images Q Tbn 3aand9gcqing6eeia Accwon4arcpibc1ipeo7otdak8ipb5e0uo00hj6m Usqp Cau

5 Most Overlooked Rental Property Tax Deductions With Images Rental Property Management Rental Property Investment

Pin By Latrice Davis On Beautiful Homes In 2020 Barn House Plans Barn Style House House Exterior

Outrigger Residence Anders Lasater Architects Space Proportion Light Material Archit Garage Door Design Mid Century Exterior Traditional Home Exteriors

Ocala Property Management Blog Real Property Management Diversified

Tax Depreciation Schedule Trail Creek Farm

Source : pinterest.com